Same As It Ever Was

At Davis Rea, we are continually assessing the strengths of the businesses we own. We analyze quarterly reports, attend management presentations, and evaluate industry research alongside the opinions of a diverse group of professionals who study the sectors and companies we consider for investment. The volume of available information is vast. The tools we use to scrutinize this data (yes, we use AI) and the qualifications of the people performing the work continue to grow at warp speed.

However, in my 40 years of investing, I have learned that the most important ingredients for success never change: judgment, patience, humility, and balance. One could even say that success is simply the art of avoiding the "Seven Deadly Sins" of investing.

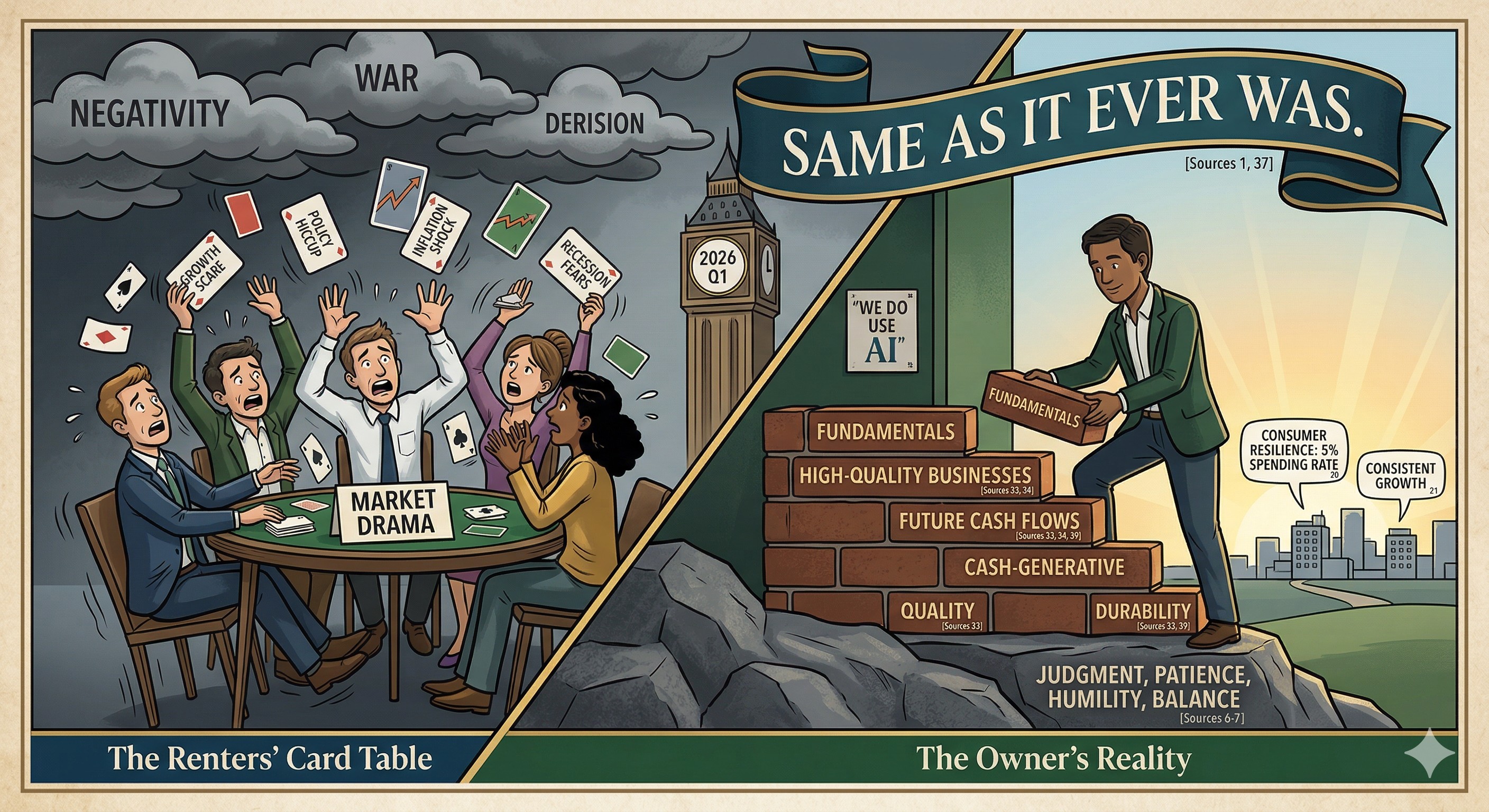

As we close the first quarter of 2026, investors are being bombarded with negativity. War, political division, and social derision are merely the icing on a cake of worries that Mr. Market is struggling to digest. Will high energy prices reignite inflation and halt the path toward lower interest rates? Will the economy tilt into a recession, causing consumers to pull back and corporate profits to fall? And what will AI mean for humanity—let alone the companies we own?

The Facts

1. Recessions are remarkably rare. We have seen only three recessions in the past 36 years. In total, they lasted 29 months, or 7% of the time. Notably, the recession that ended in 2009 accounted for half of those 29 months.

Today, energy prices are in line with levels seen in 2022 and 2025; on both of those occasions, the predicted recession failed to materialize. Interest rates rose rapidly from zero in 2022 to where they sit today. While stocks initially fell as investors feared doom, they recovered quickly during the corrections of 2022 and 2025. In fact, 2023, 2024, and 2025 were excellent years for long-term investors.

We do not see a recession in the cards. Here is what two leading CEOs had to say last week:

• Bank of America’s CEO: "Regarding consumer clients, they're still spending at a 5% year-over-year rate. It's about equivalent to last year."

• The CEO of Visa: "We’re obviously living through some tumultuous times right now. But I have to say, the watchwords for the consumer... are stability and resilience... We're just seeing consistent growth performance quarter in, quarter out, month in, month out."

2. AI is simply the next iteration of technological evolution. Innovation has influenced humanity and business valuations throughout history. Will there be losers in the future? Most assuredly. But that does not imply a "mass extinction" of software companies. Investors habitually overestimate the immediate impact of change and then underestimate its long-term significance—particularly when the change happens fast and they do not feel like "experts." Market mood swings are faster, and often of a far greater magnitude, than actual profit swings.

The fact is, we are more resilient than we feared. From a global pandemic and supply chain disruptions to hyperinflation, interest rates jumping from zero to 5.5% in six months, regional banking panics, debt ceiling standoffs, and multiple wars—the economy and the markets have seen it all. And yet, we are still here. More importantly, the economy, its companies, and its consumers have become more "anti-fragile" with each challenge.

So Why All the Drama?

At Davis Rea, we distinguish investors into two classes: "renters" and "owners." Renters treat stocks like trading cards, fleeing at the first sign of a "growth scare" or a policy hiccup. Owners, however, understand that we are purchasing a share of a company’s future cash flows. While the renters are currently panicking over the latest inflation shock or the next "word" from Washington, we are focused on the fundamental durability of the businesses we own.

This is exactly what the people running these companies are doing; they see customers buying their goods and services at ever-increasing rates. Profits are rising, yet the prices at which we can own these great companies have come down. The drama is happening at the trading card table. We shop at the bargain store.

As we close out the first quarter of 2026, I am reminded of the David Byrne line: "Same as it ever was." Today, we find ourselves in the familiar cycle of swings between manic optimism (which heralds poor future returns) and the kind of pessimism we see today—the kind that makes for great headlines, but even better long-term returns.

Final Thought

"Mr. Market" is currently trying to "front-run" a recession that the consumer refuses to participate in. We remain focused on owning high-quality, cash-generative businesses. If the "renters" want to sell us great companies at a discount, we are more than happy to be the buyers.

Long-term thinking is not just a strategy; it is our competitive advantage.

John O'Connell